Develop Digital Islamic Banking & Financing System: Cost, Process, and Features

Banks, fintech startups, and lending firms now need digital systems that support trust, transparency, and Shariah governance at every step. Users expect simple account access with fast financing journeys. Traditional banking platforms often fail to support Islamic finance logic because they rely on interest based workflows.

A digital Islamic banking system solves this gap with compliant financing models, approval controls, and customer friendly digital access. It helps financial institutions manage products with better clarity and stronger governance. It also supports users who want financial services that match their values.

Islamic banking software development gives these businesses a structured way to launch secure digital services. Through this detailed guide, businesses can understand the cost features, process, and key planning steps needed to build a digital Islamic banking and financing system.

What Is a Digital Islamic Banking and Financing System?

A digital Islamic banking system helps banks, fintech startups, and lending firms manage Shariah aligned financial services through secure online platforms. It supports digital account opening and customer onboarding. Financing requests, payments, and compliance checks can be done through one connected system. Users can easily apply for financing and upload documents. They can review terms, make payments and track account activity through a web or mobile app.

Moreover, internal teams can review applications and approve contracts to maintain audit records with better control. The system also helps financial institutions manage Islamic financing models with clear workflows and transparent product rules. This creates a smoother digital experience for users and a more structured operating model for the business.

How Islamic Banking Software Differs From Conventional Banking Software

The digital Islamic banking system works with a different product logic than conventional banking systems. It does not use interest based workflows. It supports asset backed financing, profit sharing rules, and Shariah review layers. This makes the system more structured for banks, fintech firms, and lending companies that offer Islamic financial products.

Shariah compliant banking software also helps teams manage approvals and contract terms. They can manage payment schedules and compliance checks with better control. Businesses planning broader Islamic finance products can also explore Shariah compliant platform development to manage governance workflows and approval records across different finance models.

| Area | Conventional Banking System | Islamic Banking System |

| Revenue logic | Interest based model | Profit sharing or asset based model |

| Loan flow | Direct lending | Contract based financing |

| Compliance | Regulatory checks | Regulatory plus Shariah checks |

| Product setup | Standard financial rules | Product rules linked to Islamic contracts |

| Audit need | Financial audit | Financial and Shariah audit |

Core Islamic Financing Models Your System Should Support

A strong platform should support different Islamic finance models with clear product logic. Each model needs its own approval path, contract rules, payment flow, and reporting structure. Islamic financing software helps financial institutions manage these models with better accuracy and less manual work.

1. Murabaha Financing Workflow

Murabaha supports asset based financing. The system records the asset request, purchase cost markup approval, and installment plan. It also tracks customer consent payment status and ownership transfer once the contract terms are complete.

2. Ijarah Leasing Workflow

Ijarah supports leasing based finance. The system manages asset details and usage rights. Rental schedules, due dates, and renewal terms can also be handled efficiently. It can also support ownership transfer options when the lease ends.

3. Musharakah Partnership Workflow

Musharakah supports partnership based financing. The system records partner contributions, profit ratios, loss sharing rules, and project performance. It also helps teams track reports, payouts, and account updates with full visibility.

4. Mudarabah Investment Workflow

Mudarabah supports investor and manager based investment. The system records investor capital manager responsibilities, profit sharing terms, and business performance. It helps teams manage returns, report approvals, and risk visibility.

5. Takaful and Zakat Support

Takaful means Islamic insurance support. Zakat means charitable giving and support. The platform can include optional modules for contribution tracking, claim workflows, Zakat calculation records, and user reporting when the business model needs them.

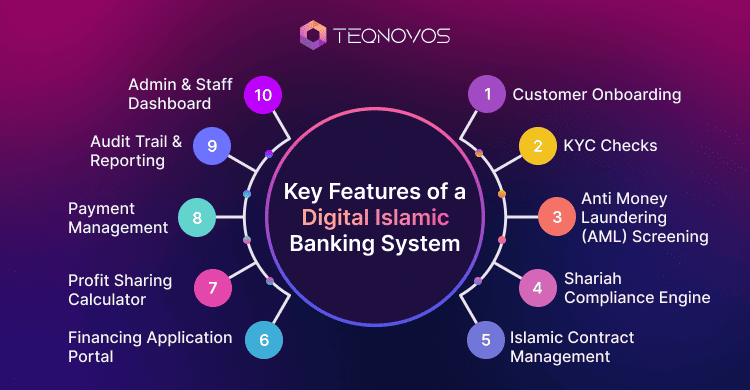

Key Features of a Digital Islamic Banking System

A digital Islamic financing software needs more than account access and basic payments. It should support key features such as user onboarding, financing flows, contract rules, and compliance checks with secure operations. The right features help users move faster.

1. Digital Customer Onboarding

Islamic digital banking solutions make onboarding faster by reducing branch visits and manual paperwork. The system collects personal details and identity documents through one secure system. It also helps staff review applications faster and reduce incomplete submissions.

2. KYC Checks

The system checks user details, documents, and risk profiles before account activation to verify user identity. This helps banks and fintech firms protect the platform and meet compliance requirements.

3. Anti Money Laundering (AML) Screening

AML screening means checking transactions against financial crime risks. The system screens users’ activities and payment behaviour for suspicious patterns. It can also flag high risk actions for staff review before approval.

4. Shariah Compliance Engine

A Shariah compliance engine helps teams manage product rules and contract logic. It can check prohibited activities, financing conditions, approval paths, and documentation needs. This keeps financial products aligned with internal policy and Shariah governance standards.

5. Islamic Contract Management

Contract management helps teams create and approve Islamic finance agreements. They can easily sign, store, and renew Islamic finance agreements. The system can manage Murabaha, Ijarah Musharakah, and Mudarabah contract templates. It also keeps every version and approval record ready for audit.

6. Financing Application Portal

A financing portal lets users apply for products through web or mobile access. Users can upload documents, review terms, track status, and receive updates. Internal teams can review applications, assign approvals, check risk, and manage disbursement steps.

7. Profit Sharing Calculator

A profit sharing calculator helps manage partnership based finance models. It calculates investor share, partner ratios, business returns, and payout records. This gives users clear visibility and helps teams avoid manual calculation errors.

8. Payment and Installment Management

Islamic financing software helps in tracking payment schedules, receipts, overdue amounts, and contract status in one place. The system can send reminders, process payments, and flag overdue amounts. It also helps staff monitor collection status without switching between tools.

9. Audit Trail and Reporting

Audit trails record every approval change transaction and compliance action. Reports help teams review financing performance, user activity risk alerts, and Shariah governance records. This gives financial institutions stronger control during audits and internal reviews.

10 Admin and Staff Dashboard

A Digital Islamic banking system should give staff clear visibility into approvals, users, and financing activity. Teams can easily manage user roles and update application status. They can also track platform activity. This improves daily operations and decision making.

11. Mobile Banking App

A mobile app gives users access to account transfers and repayment notifications. Islamic banking app development should focus on simple user journeys and secure access for clear contract visibility. This helps users manage financial activity with confidence through digital channels.

Note: Businesses can also use AI software development services to support fraud checks, risk alerts, and smarter reporting.

Build a Shariah Ready Banking Platform —launch secure Islamic banking software with compliant workflows.

Schedule a CallTechnology Architecture for Islamic Banking Software

A strong architecture keeps the platform secure and scalable. It connects users, staff, and financing workflows through clear system layers. Islamic core banking software also needs flexible integration support so banks and fintech firms can connect existing systems without disrupting daily operations.

1. User App Layer

Islamic banking app development makes account access, document upload, and financing requests simple for users. They can also review contracts and make payments.

2. Admin Portal Layer

The admin portal layer helps staff manage user applications, approvals, and support requests. It gives teams a central view of daily operations and pending actions.

3. Financing Workflow Layer

The financing workflow layer manages product journeys for Murabaha, Ijarah Musharakah, and Mudarabah models. It controls approvals, rules payment schedules, and contract status.

4. Shariah Compliance Layer

The Shariah compliance layer applies product rules, contract checks, and review workflows. It helps teams validate financing actions before approval and keeps records ready for audit.

5. Core Banking Integration Layer

This layer connects the platform with existing banking systems. It helps sync account data, customer records, transaction history, and balance updates through secure system connections.

6. Payment Integration Layer

A Shariah compliant finance app needs secure payment flows for transfers, repayments, and receipts. It can connect with payment gateways, bank rails, and digital wallets based on business needs.

7. Reporting and Analytics Layer

Islamic digital banking solutions turn financing data into clear reports for better decisions. Teams can explore AI solutions for fintech to improve risk monitoring, reporting, and user activity insights.

8. Security Layer

Security planning is important in Islamic banking app development because users share sensitive financial data. It uses encryption role based access, audit logs, fraud checks, and secure authentication.

9. Application Programming Interface Layer

Application Programming Interface means a secure connection that lets two systems share data. This layer helps the platform connect with identity checks, payment tools, accounting systems, core banking systems, and reporting tools.

Cost to Develop an Islamic Banking and Financing System

The cost of an Islamic banking software development usually depends on the scope, features, compliance depth, and integration needs. A basic portal costs less. A full banking system costs more because it needs advanced workflows, secure architecture, and multiple system connections.

Note: Islamic fintech platform development should always be estimated by module and business goal rather than one fixed price.

| System Type | Estimated Cost Range |

| Basic Islamic banking portal | USD 40K to USD 80K |

| Mobile app with financing workflows | USD 80K to USD 150K |

| Full digital Islamic banking system | USD 150K to USD 350K |

| Enterprise level platform | USD 350K to USD 700K plus |

Key Cost Factors

-

Number of User Roles

The cost increases when the platform needs separate access for customers, staff managers, auditors, and Shariah reviewers. Each role needs its own dashboard permissions and workflow controls.

-

Financing Models

Murabaha, Ijarah, Musharakah, and Mudarabah need different rules. Each model needs separate application flows and payment schedules.

-

Shariah Compliance Rules

The system needs approval paths, product rules, and prohibited activity checks. Stronger governance needs more planning, testing, and validation.

-

Mobile App Scope

A simple app may only support account access and payments. A larger app may include financing requests, document upload notifications, repayment tracking, and customer support.

-

Core Banking Integrations

Integration with existing banking systems can affect cost. The platform may need to sync customer data, account balances, transaction records, and approval updates.

-

Security Needs

Banking platforms need strong protection. Cost can increase with encryption and access control. Advanced security features like fraud checks, secure login, and audit logs may increase the overall cost.

-

Reporting Requirements

Basic reports cost less. Advanced dashboards cost more because they track financing performance, user activity, and risk alerts.

-

Region Specific Compliance

Each market can have its own financial rules. The platform may need local reporting formats, data storage rules, and identity checks.

-

Post Launch Support

Support costs depend on the platform size. The system may need performance monitoring, bug fixes, security updates, and feature upgrades after launch.

How to Develop an Islamic Banking and Financing System: Step-by-Step Process

A clear process helps teams reduce risk and build the platform with better control. Islamic fintech platform development needs early planning because each feature must support user needs, compliance rules, and Shariah governance.

1. Requirement Discovery

Shariah compliant banking software needs clear product goals before design and development begin. Therefore, in this stage, teams define what the platform should support for customers, staff, and Shariah reviewers.

2. Shariah Product Mapping

Each financial product needs a clear Shariah logic before development starts. Teams map Murabaha, Ijarah, Musharakah, Mudarabah, or other models into digital workflows.

3. Compliance Workflow Planning

The platform needs approval paths, review steps, and audit records. This stage defines how users submit data and how internal teams approve each action.

4. User Experience Design

Designers create simple journeys for onboarding, financing payments, contracts, and support. The goal is to make complex banking actions easy for users.

5. System Architecture Design

This stage also helps teams align Islamic banking software development with future product growth and compliance needs.

6. Module Development

Developers build core modules such as onboarding, financing contracts, and payments dashboards. Each module should follow the approved workflow.

7. Integration Setup

The platform connects with core banking systems, payment gateways, identity tools, and reporting systems. These connections help teams avoid manual data entry.

8. Security Testing

Strong testing makes Islamic banking software development safer for users, staff, and financial records.

9. Shariah Review and Validation

Shariah reviewers check product logic, contract flows, and approval records. This step helps confirm that the system supports the intended governance model.

10. Pilot Launch

Pilot testing helps teams check if Shariah compliant banking software supports real user and staff workflows. Teams can review performance, user feedback, errors, and approval delays before full release.

11. Full Platform Rollout

Full rollout helps teams scale Islamic digital banking solutions across users, products, and internal operations. Teams monitor onboarding, financing payments, reports, and support requests during the early launch stage.

12. Post Launch Improvement

Post launch updates help improve Islamic banking app development flows after real user feedback. Any changes regarding compliance and performance improvements can be made in this stage. This not only keeps the system useful but also secure and ready for future growth.

Common Challenges in Islamic Banking Software Development

Islamic banking software development needs careful planning because they combine finance rules, user journeys, and compliance checks. These challenges can affect cost, timeline, and launch quality. Businesses can review fintech app security solutions to reduce risks around data access, payments, and audit records.

Adding Shariah Rules Too Late

- Late rule mapping can force teams to rebuild product flows.

- Contract logic may need major changes after development starts.

- Approval steps can become unclear for staff and Shariah reviewers.

- Early Shariah planning helps reduce rework and launch delays.

Handling Multiple Islamic Financing Models

- Murabaha needs asset purchase markup and installment logic.

- Ijarah needs lease terms, rental schedules, and ownership options.

- Musharakah needs a partner contribution profit ratio and loss sharing rules.

- Mudarabah needs investor capital, manager roles, and return tracking.

Connecting With Legacy Banking Systems

- Older systems may not support smooth data exchange.

- Customer records can become duplicated across platforms.

- Transaction updates may move slowly between systems.

- Strong integration planning helps reduce operational gaps.

Managing Manual Document Workflows

- Manual document collection can slow user onboarding.

- Contract review can take longer without digital approval flows.

- Missing files can delay financing decisions.

- Digital storage helps teams track documents with better control.

Maintaining Audit Ready Records

- Each approval should leave a clear system record.

- Contract edits should show version history and reviewer details.

- Payment actions should connect with financing records.

- Strong audit trails support both financial and Shariah reviews.

Balancing User Experience With Compliance

- Users need simple forms and clear next steps.

- Compliance teams need detailed checks and review points.

- Long processes can increase drop offs during onboarding.

- Smart workflow design keeps the journey smooth and controlled.

Planning Cost Without a Clear Scope

- Unclear features can lead to weak budget estimates.

- Missing integration details can increase cost later.

- Extra financing models can expand development time.

- A defined scope helps teams plan the cost timeline and launch phases.

Turn Islamic Finance Into a Digital Experience —build secure onboarding financing and Shariah review workflows.

Schedule a CallHow to Reduce Development Cost Without Weakening Compliance

Businesses can reduce development costs with better planning. Cost control should not weaken Shariah governance security or audit readiness. The right approach helps teams launch faster and protect the platform from expensive changes later.

Start With Priority Modules

- Build the most important modules first.

- Focus on onboarding, financing contracts, payments, and admin controls.

- Move advanced reports and extra features to later phases.

Launch One Financing Model First

- Start with one core model, such as Murabaha.

- Build its full workflow with contract logic and approval steps.

- Add Ijarah Musharakah or Mudarabah after the first model works well.

Use Reusable Contract Templates

- Create approved templates for common financing products.

- Reuse contract fields, clauses, approval flows, and storage rules.

- This reduces manual document work and future development effort.

Plan Integrations Early

- List all required systems before development starts.

- Include payment gateways, identity tools, core banking systems, and accounting tools.

- Early planning helps avoid data flow issues later.

Build Compliance Into the First Architecture

- Add Shariah rules and compliance checks during early planning.

- This avoids costly changes after development begins.

- It also keeps the system ready for review.

Test Workflows Before Full Rollout

- Testing a Shariah compliant finance app helps teams fix user journey gaps before launch.

- Check where users face delays or confusion.

- Fix process gaps before the full launch.

Conclusion

A digital Islamic financing software helps banks, fintech firms, and lending companies deliver secure and transparent financial services. It supports compliant workflows, clear contracts, payment tracking, and audit ready records.

Businesses can reduce risk by planning user roles, financing models, integrations, and compliance needs before development starts. A clear roadmap helps control cost, improve launch quality, and support long term platform growth.